.svg)

.svg)

Targeted support creates a new middle ground that enables regulated firms to provide ‘ready-made suggestions’ to groups of customers with common characteristics who share a similar support need or objective (FCA).

It is intended to fix three related problems in UK financial advice:

- Firms have been nervous of breaking the advice rules. Under the old regulation, firms often worried that giving anything more than generic information could be treated as a personal recommendation. When combined with past mis-selling scandals, that made many financial firms nervous of doing the wrong thing and wary of offering anything that looked like advice to help customers, stifling innovation.

- People turn to alternative sources of advice. About 7 million adults in the UK hold £10,000 or more in cash savings. Among non-advised consumers with over £10,000 of investible assets held solely in cash, many want more support to make decisions. Since this need remains unsolved by regulated financial firms, people turn to unregulated financial guidance, tips and advice available through social media and now AI. This leaves consumers exposed to unregulated and potentially harmful financial ‘advice’ from people promoting dubious investment schemes.

- The UK government wants better long-term financial outcomes and a stronger retail investment culture. The FCA has linked targeted support to helping consumers make better-informed saving, pension and investment decisions, and to broader efforts to encourage more appropriate retail investment.

Targeted support enables firms to offer customers the financial guidance that many have sorely needed. But with customers increasingly moving on to general-purpose AI and other sources of guidance, firms face two challenges: understanding the new decision making journey and implementing targeted support propositions that are compliant, genuinely helpful, and commercially valuable.

Segmentation is mandatory, but good segmentation is where the value is created

The FCA requires firms to define the customer segment in advance and specify a single ‘ready-made’ suggestion for that segment before delivering it. This makes targeted support deliberately for segments of customers with common characteristics who share a similar need or objective, rather than a fully individualised recommendation. The questions are which groups, for which decisions and how to identify them.

For targeted support, the FCA says that:

- Segments should be based on a shared financial support need or objective.

- Firms must define who is included and who is excluded from the segment.

- Segments must be detailed enough to support a ready-made suggestion, but not so detailed that they become a full individual assessment.

This creates the Goldilocks challenge: firms need segments that are not so broad that the suggestion becomes generic, but not so narrow that the journey becomes a personalised assessment. The segment has to be “just right” for one ready-made suggestion to be reasonable.

Identifying the “just right” segmentation

Research for the Association of British Insurers (ABI) identified robust consumer segmentation as one of the top three risks insurance and pension firms face in implementation. To make the support offered genuinely helpful, firms need to define who the support is for, why that group shares a common need, and why a ready-made suggestion could reasonably leave them in a better position.

Firms need to get segmentation right because the value of targeted support depends heavily on it. Well-defined segments:

- Turn advice gaps into support opportunities. Millions of customers who do not have access to personal financial advice need more than generic information. Well-defined segments enable firms to give these customers support that is relevant, timely and decision-specific, without requiring a full individual advice process.

- Differentiate targeted support from unregulated sources through customer context. As customers increasingly turn to AI, social media and other sources, targeted support gives regulated firms the opportunity to provide recommendations that are more contextual and accountable. Financial firms have the advantage of regulated access to verified customer data, product expertise, and compliance infrastructure. By translating customer data into meaningful segments and product context into ready-made suggestions, firms can identify shared support needs and differentiate targeted support from generic, unverified guidance.

- Enable firms to build scalable, commercially valuable propositions. The more accurately the segment reflects a real customer decision need, the more relevant the prompt and ready-made suggestion becomes, increasing the likelihood of engagement and action. This can support retention, asset growth, increased contributions and lower-cost support for customers who may not be economical to serve through full advice.

Using Jobs to be Done to strengthen your customer segmentation

One useful way to think about a “financial support need or objective” is through the lens of Jobs To Be Done: the progress a customer is trying to make towards their goal or aspiration, and the decision they need help resolving in a particular situation. Considered alongside demographic and financial situation data, Jobs theory helps firms ensure targeted support recommendations also align to customers’ desired outcomes.

A strong targeted support segment is one where the firm can say: “These customers share a clear financial situation, and the same ready-made suggestion will help them make progress towards a shared Job to be Done.”

You should be able to say yes to the following check list:

Situation: Does the segment describe a clear customer situation, including any life-stage context that affects the decision?

Jobs to be Done: Do you have clarity on the shared JTBD within this segment and the ready-made suggestions that might help customers to progress towards it?

Boundaries: Does the segment define the right inclusion and exclusion criteria?

Suggestion: Is the segment specific enough to support a ready-made suggestion, without becoming a full individual assessment?

What we can learn from early targeted support providers

With the first propositions now being deployed, we can begin to see how early adopters are implementing their segmentations:

1. Using observable data and reasonable assumptions. Legal & General focuses on customers whose pension savings are fully invested in cash. This creates a clear signal: a long-term savings product is being held in a short-term, low-growth asset. Based on observable data such as age and pension allocation, Legal & General can reasonably assume that some customers in this group may benefit from considering whether part of their pension should be moved into longer-term investment options.

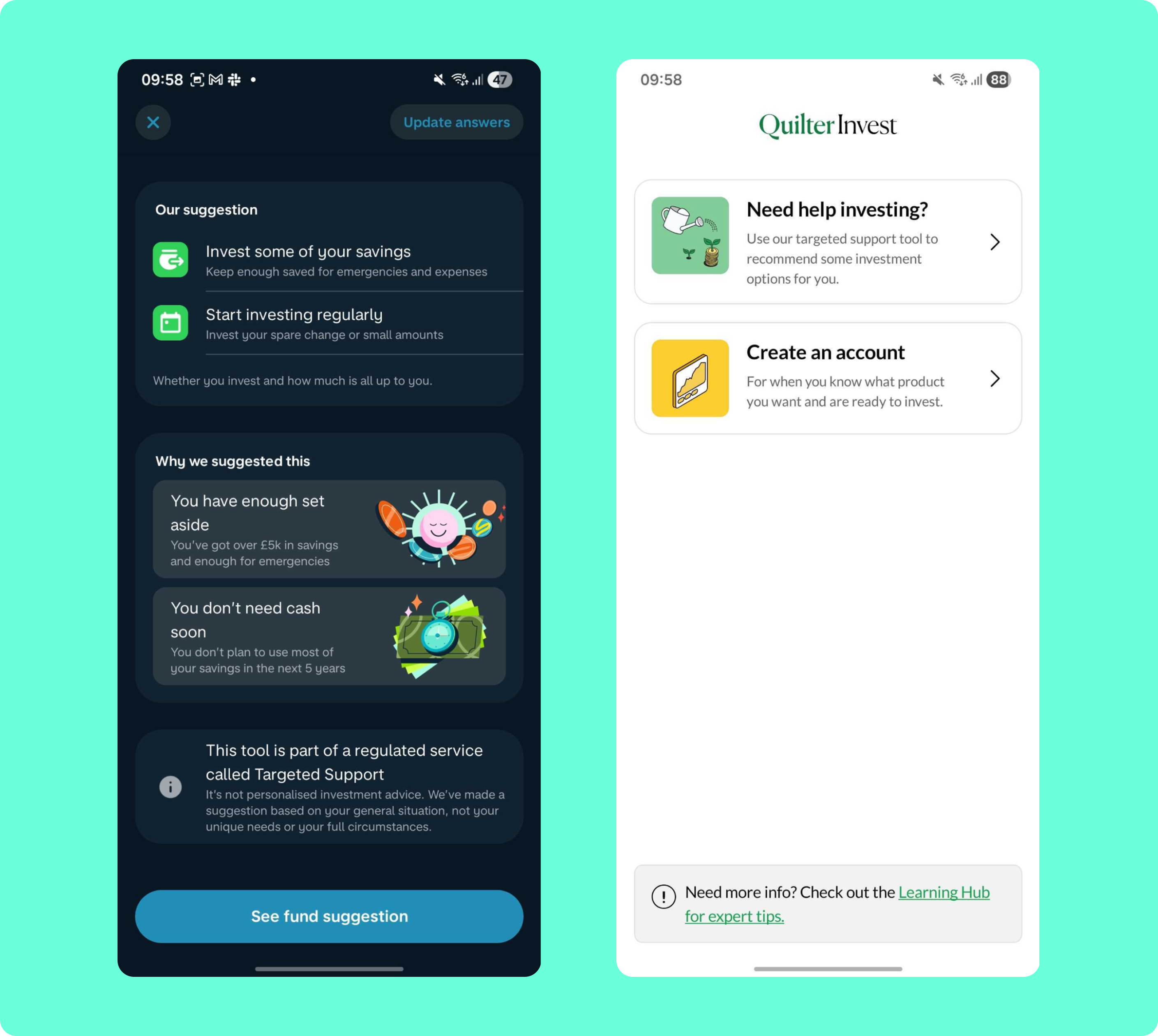

2. Asking customers clarifying questions to gather information, validate data and assumptions. Monzo's questionnaire (below) checks whether customers have a sufficient emergency buffer based on their monthly expenses, no short-term need for the money and a risk preference that can be matched to an investment option. Meanwhile, Quilter Invest wants to support people in the earlier stages of their investing journey, so it shows its targeted support prompt even before a prospect creates an account. It uses a questionnaire (below) to gather prospects’ information before showing a targeted support suggestion.

3. Using AI to infer likely JTBD or desired outcome, aligning customers to pre-defined segments and ready-made suggestions. Scottish Widows is already expected to test AI-enabled targeted support with the FCA, along with eight other firms, including Barclays, Experian, and UBS, to support safe and responsible deployment. AI can help firms analyse customer data and infer likely JTBD, ask clarifying questions, explain a suggestion more conversationally, and align customers to the right segment using existing or newly collected information. But firms cannot use AI to generate a different recommendation for every customer in real time, as it will fall into advice territory.

Where we believe targeted support should go further

Targeted support has the potential to bridge the advice gap, but its success will depend on how well firms define and operationalise customer segments.

The strongest propositions will go beyond basic traits such as age, balance or product holding, and use JTBD thinking to identify the financial decisions a group of customers need help resolving.

In the first iteration, targeted support may still focus on specific product, investment or pension decisions. But as it matures, JTBD can help firms frame the ready-made suggestion, explain the assumptions and caveats, and design segment-based follow-up journeys that move customers towards achieving their goal. This will be essential to make the recommendation more useful for customers, while supporting stronger engagement and retention for firms.

As firms test these propositions, continuous dialogue with regulators will be essential to turn targeted support from a regulatory permission into a genuinely valuable customer experience.

We help financial institutions create future growth engines

At 11:FS, we don't just design digital propositions; we help you navigate the complexity of the growth cycle - from validating unmet customer needs to launching scalable future ready propositions.

If you are struggling to define whether targeted support presents a genuine product opportunity for your firm, let’s talk.