.svg)

.svg)

.png)

When I bought my first house, I discovered I needed to pay Chancel Repair Liability (CRL). This legally enforceable obligation requires property owners in England and Wales to fund repairs to a local parish church's chancel. In the UK, buying a home involves a series of unwelcome surprises: surveys, legal fees, searches, mortgage fees, removals.

The catch? You don't realise how expensive costs are until they compound. The problem is not just that buying a home is expensive, but that the costs are hidden and badly sequenced.

Financial services should be designing products and services that help buyers understand all of the costs involved in their end-to-end financial journey before committing.

Stamp duty

Stamp duty is a tax you pay to the government when buying a house in England. It hits buyers at the point of maximum financial strain and is one of the first major financial blows in a series of cash-flow shocks.

Some costs appear before completion, such as conveyancing and legal fees, but other recurring charges only emerge after moving in. That is not just a policy problem; it is a communication failure. Lenders, brokers and banks should be working together to guide homebuyers through the entire journey and surface costs earlier.

The hidden-cost sandwich

Buildings insurance, utilities, broadband and repairs arrive in quick succession. For leaseholders and share of freeholders, service charges and management fees compound further. The Mortgage Advice Bureau estimates hidden costs for a first-time buyer could exceed £18,000 on top of the deposit.

Similar issues persist beyond the UK. Research conducted by 11:FS in 2022 for a Canadian credit union found that pain points are acutely felt pre- and post-purchase, and that customers are increasingly seeking tools and services that address the ongoing financial commitment of ownership.

Never moving, always renovating

Increasing costs push buyers to lower search budgets, skip surveys, and settle for worse properties. The more financially stretched the buyer, the more likely they are to underinvest in checking the home and inherit expensive problems later. People who feel blindsided are less likely to move, borrow confidently, or engage with the wider market.

Other countries, like the US and the Netherlands, levy annual property taxes rather than stamp duty, incentivising regular moves. The UK's stamp duty creates the opposite effect. Millions live in homes too large for their needs. This makes downsizing harder, mortgages less dynamic, and market entry harder for younger buyers. A better financial services layer could ease this friction by showing affordability across the full ownership lifecycle.

New rules, same problem

Recent government reforms require upfront information from sellers and estate agents, mandating digital identity checks and qualifications to reduce fraud and time to purchase. These regulations address information gaps, but they do not address pre- and post-purchase cost burdens. The untapped opportunity lies in joined-up financial support for move-in and ownership costs.

The 11:FS home-buying report details how many fintechs and proptechs are starting to stitch together disparate services for customers, treating home-buying as a continuous journey rather than a stack of disconnected tasks.

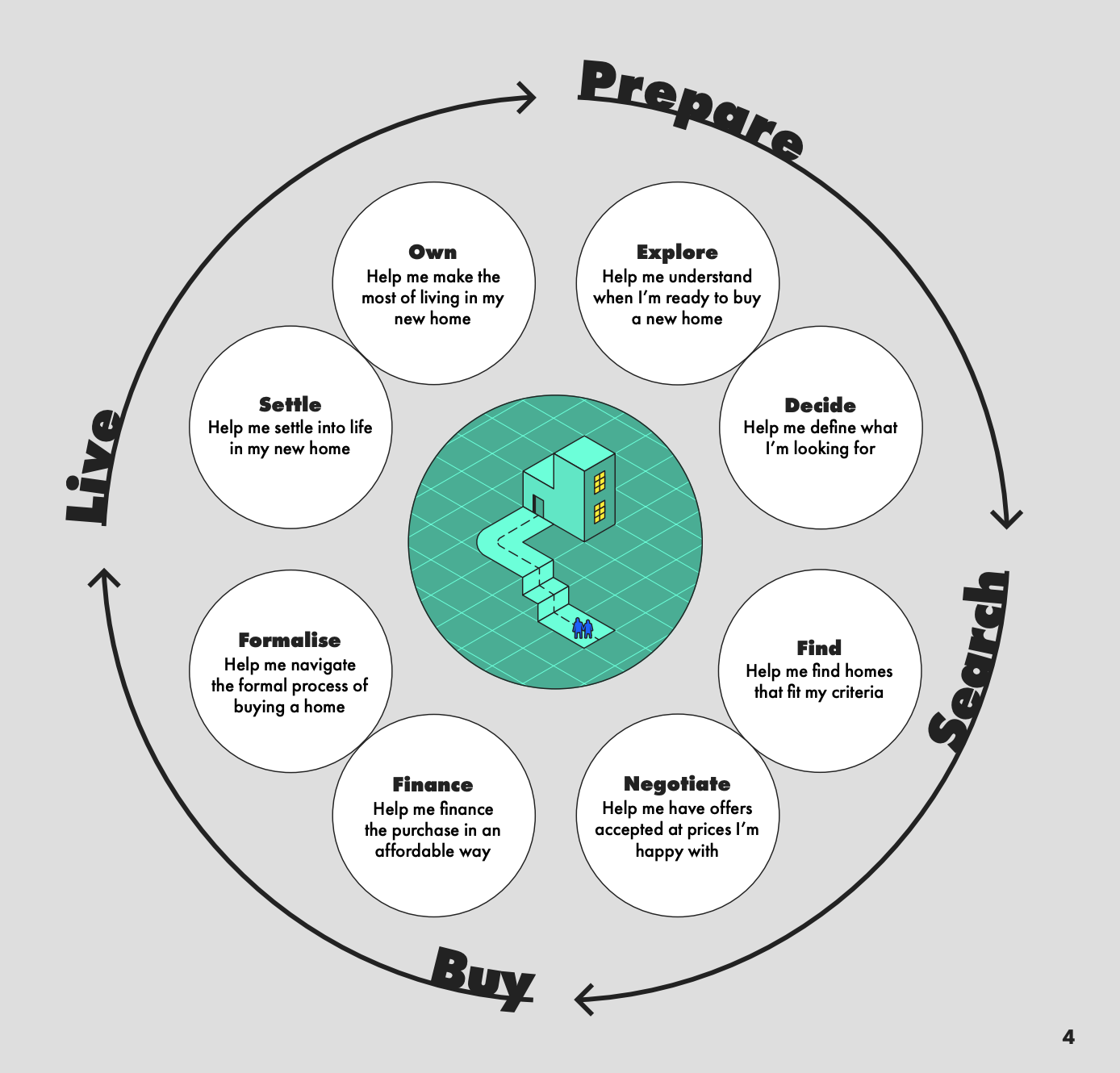

Who is doing it well?

Home-buying has historically been broken into fragments: an app for searching, a calculator for stamp duty, a solicitor portal, and an insurance quote journey. The best players are the ones trying to stitch the journey together.

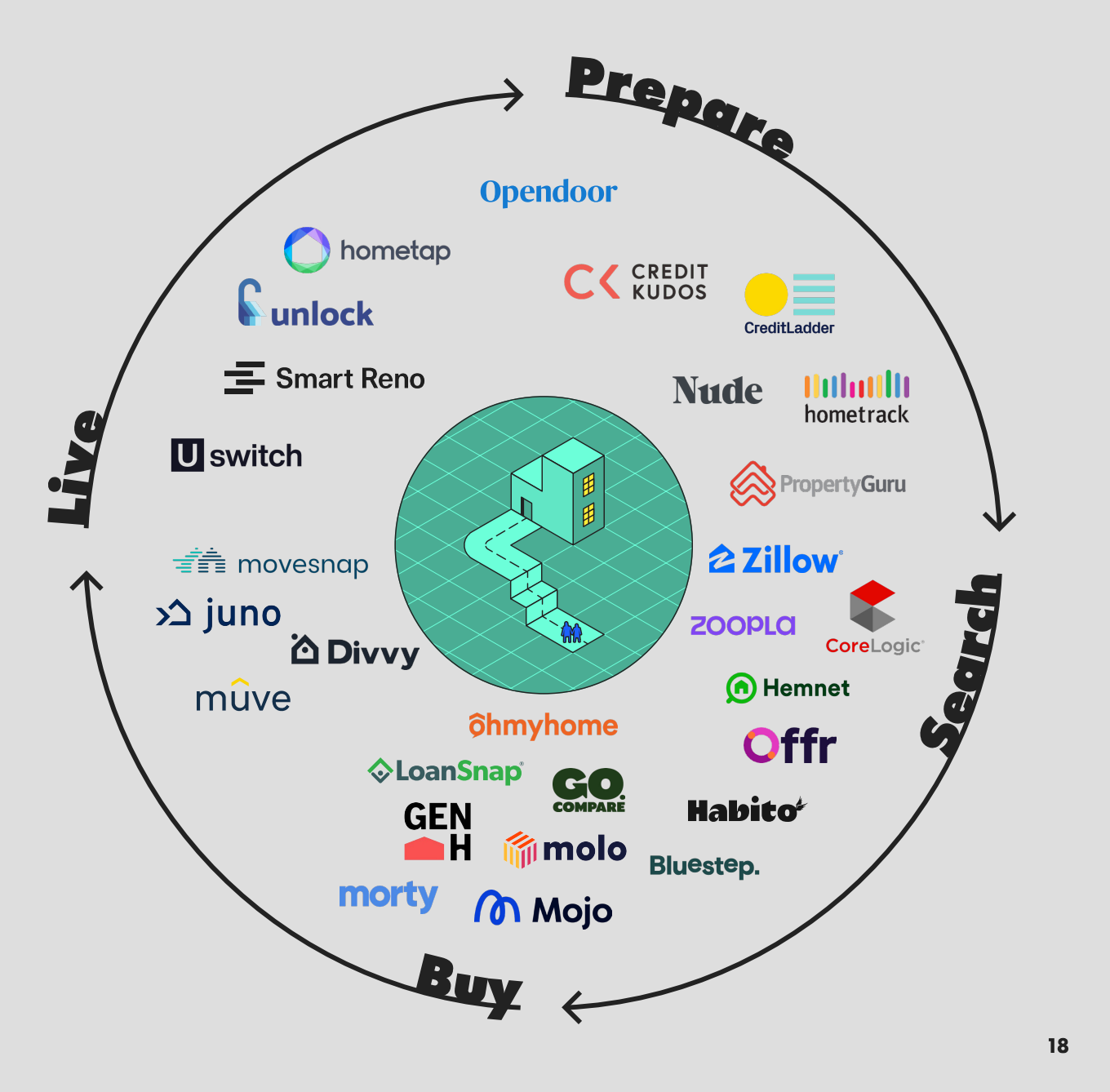

HNTR combines house-hunting, cost tracking, and purchasing checklists in one app. Mojo Mortgages has built a digital ecosystem integrating budgeting, open banking insights, mortgage discovery, and transparent credit scoring. However, the market remains under-designed.

The missing product

The market gap is in ownership planning. Banks and financial institutions that treat home ownership as a continuous financial relationship will capture wallet share across insurance, utilities, savings, and refinancing. The competitive advantage goes to institutions that show the full cost picture upfront and support customers through the ownership lifecycle.

Buyers need to know their monthly life-cost after completion and how those numbers shift if they downsize, renovate, or refinance. Financial institutions should:

- Provide integrated pre-purchase cost calculators showing total ownership costs before offer acceptance.

- Develop post-completion financial planning tools that forecast recurring charges and lifecycle costs.

- Allow stamp duty payments to be made in increments outside the mortgage.

- Standardise service charge and management fee disclosure to enable comparison.

- Create partnerships with insurers, utility providers, and property tech platforms to deliver joined-up guidance.

At 11:FS, we can help you understand the underserved needs of homebuyers through Jobs to be Done research. We design intelligent services around end-to-end customer journeys and help you explore fintech partnerships that drive customer retention and wallet share.

Contact the team today to learn how ownership planning becomes competitive differentiation.