Content Hub

.svg)

.svg)

APIs

The virtues of digital : creating a truly digital bank

At 11:FS we like to say that digital banking is 1% finished, well the same is true of Open Banking. The unknown potential of the regulation far outstrips what is being done right now. And that potential has caught the imagination of foreign regulators.

What do we want banking to look like in 2020?

In her latest column for Forbes, 11:FS Head of Research Sarah Kocianski analyses Chime's recent outages and challengers' reliance on third-party processors.

What is PSD2 and what will it mean for customers?

Fintech Connect 2020 is just around the corner! It’s taking place online from the 30th November to the 4th December, with 8,000 attendees and more than 200 speakers already confirmed.

Banking APIs Aren't about Tech or Banking

I’m sure that you’ve seen the same presentations that I have. An expert from a large consultancy stands up and his first slide says “API stands for Application Programming Interface”. He continues with a description of new regulations (PSDII / CMA) and describes the technology that will let customers give third parties to access their banking data and trigger new transactions. That’s all true, but it’s a mistake to start there, it leads in the wrong direction.

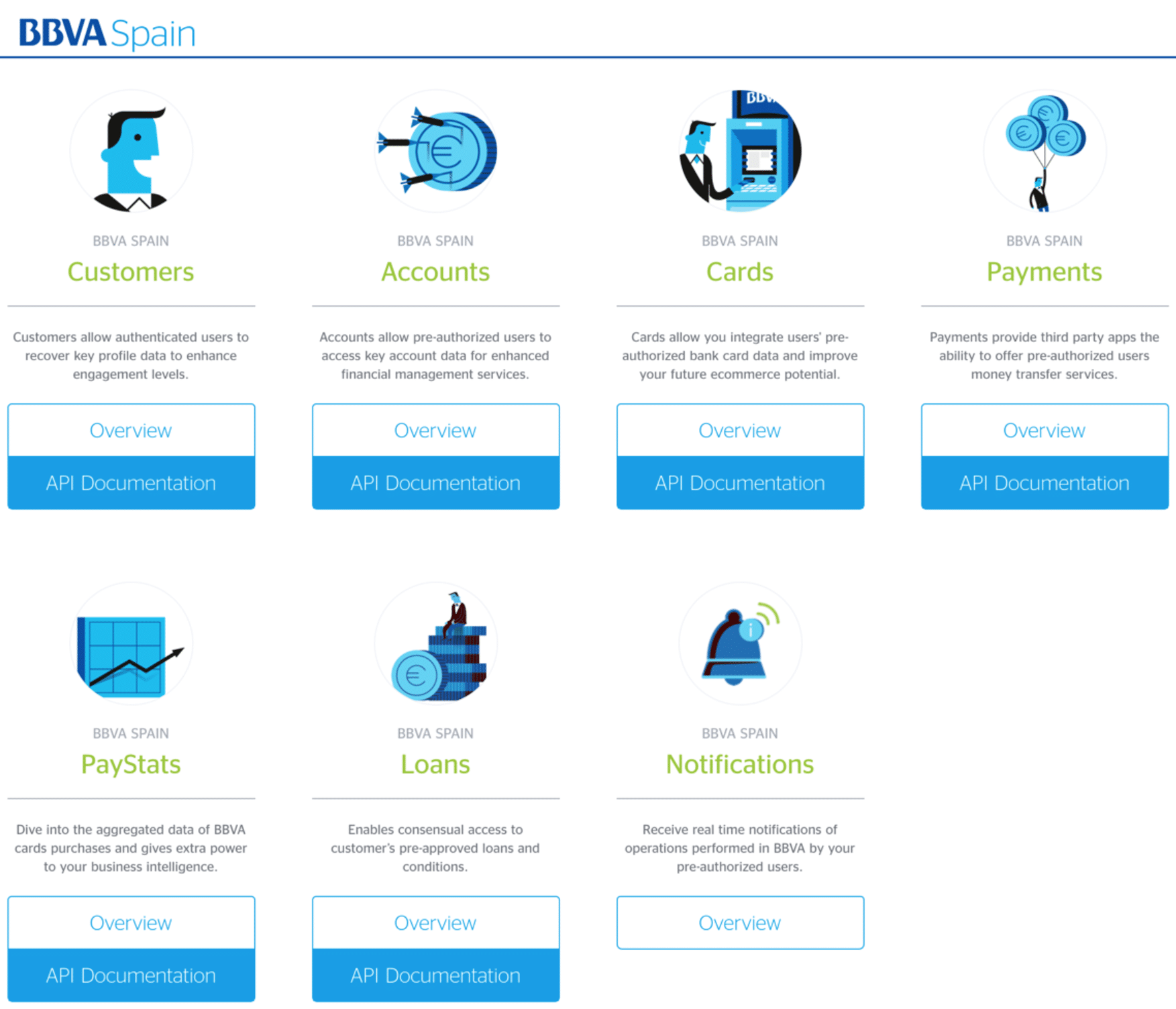

11 Banks and FinTechs Doing APIs Better Than You

In its final report, the Competition and Markets Authority has formally implemented reforms aimed at giving people more control of their money. By Q1 of 2018, European banks have to completely open up their data through full APIs. But some banks aren’t prepared to wait that long. Read on to see which ones have taken the lead.

M-PESA's Mobile Money Revolution: Key Lessons for Banks

There’s a sad truth we have to accept around AI and Machine Learning (ML). Right now neither are going to end with the sci-fi films that we all know and love. Most people hear AI or ML and immediately have that in mind, but we’re a long way off from robot companions taking over the world. The global proliferation of Human-Like Intelligence is unlikely to happen anytime soon.

FinTech Legend Leda Glyptis: If You Choose Who You Are, What You Do Will Follow

Over the past eight years, as a fintech founder who happens to be gay, I’ve met with 100+ corporate and institutional investors around the world.

The Rebundling of UK Financial Services

Death. It's inevitable. It's also a financial nightmare most don't see coming. But what if you could save tens, if not hundreds of thousands of dollars during this grim process?

Why PSD II could be the final straw to bad leadership and unblocks internal resistance to real banking innovation finally

Our CEO, David Brear, talks everything PSD 2 for HotTopics. Legislation is usually brought in to reduce stupidity amongst individuals, or groups exhibiting behaviors that may cause harm. PSD 2 is no different in terms of its purpose and overall need to exist. The European Commission has tried to foster innovation and filter banks toward more inclusive ways of working. PSD, miData and a number of other “carrots” meant to foster innovation have been used with limited success. Banks have treated all of these as purely compliance driven; tick box exercises, and tend to deliver the bare minimum to meet legislation. With regulators and governments now losing patience with banks, we now have the “go to your room” moment; PSD 2.

No items here

No items here

960

Insights: The future of Revolut with UKCEO Francesca Carlesi

The UK banking battlefield has never been more competitive. Customers expectfinancial apps that are personalised, seamless, and that genuinely make a differenc...

960

Insights: The future of Revolut with UKCEO Francesca Carlesi

960

Insights: The future of Revolut with UKCEO Francesca Carlesi

The UK banking battlefield has never been more competitive. Customers expectfinancial apps that are personalised, seamless, and that genuinely make a differenc...

960

Insights: The future of Revolut with UKCEO Francesca Carlesi

960

Insights: The future of Revolut with UKCEO Francesca Carlesi