.svg)

.svg)

Recently I had the chance to sit down with experts from Stratiphy, Cleo, and Snowdrop Solutions to discuss how ‘personalisation’ in financial services is becoming the primary differentiator for firms in retaining and deepening their relationships with customers.

This article builds on the conversation we had, discussing how new technologies are enabling personalisation today, what data and infrastructure are making it possible, and who is delivering best-in-class experiences.

What true personalisation looks like (and why it matters)

Let’s start with a definition: ‘true’ personalised experiences are distinct journeys based on when, where, and why financial decisions are made, based on the following principles:

- Have a detailed picture of a customer's behaviour: knowing when bills are due, when paychecks land, and when major life events occur. Financial firms using insights from user behaviour can nudge customers in the moment - before a late payment, or when there’s an unexpected cash flow squeeze.

- Understand the underlying context: services that understand not just what you said, but also when you said it and under what circumstances, are gaining ground. These aren’t just dashboards with graphs that people ignore, they're tools that pre-emptively offer nudges, highlight anomalies, and help users act with confidence.

- Balance simplicity and control: Many customers want control, but not complexity. They’d rather have a few well-chosen levers than dozens of confusing knobs. The best services let users input their goals (saving for a home, retirement, investing style), and then quietly do the heavy lifting behind the scenes with machine learning, while keeping the core logic transparent and trustworthy.

- Bake in trust & privacy: As firms gather more data - transactional, demographic, behavioural - the risk of veering into creepy territory increases. Customers differ greatly across markets: what’s acceptable in the UK might be concerning elsewhere. Accountability and respecting local regulations are essential.

If doing any of the above sounds hard, that’s because doing any or all of the above has been elusive for most financial institutions since the dawn of digital time. So what’s changing?

Emerging trends & regulatory shifts shaping the future

Recent developments in regulation, data policy, and technology are giving financial services firms both the tools and the guardrails to create more meaningful personalisation at scale. Here are 4 trends reshaping how data is used, how advice is delivered, and how consumers interact with their money.

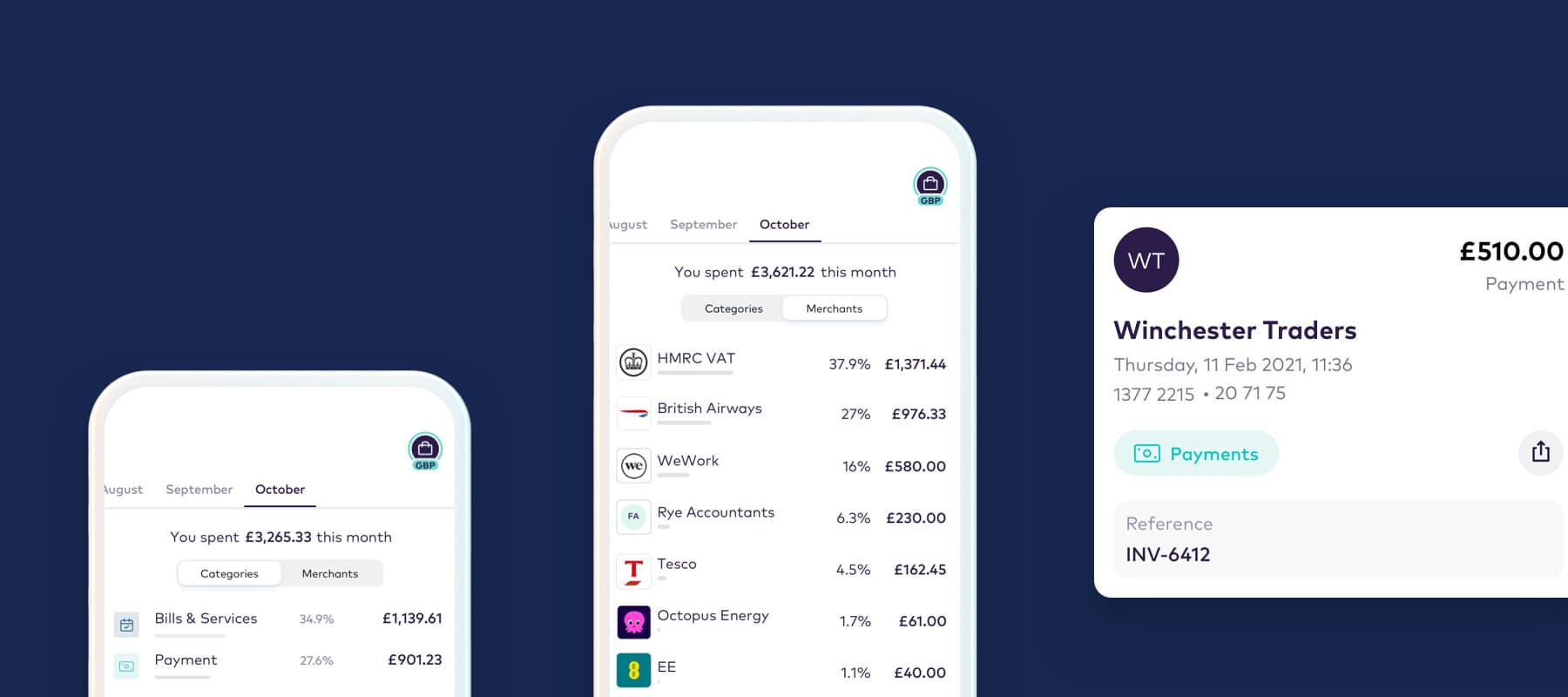

1. Richer, high-frequency data

Open banking created the first wave of consented access to balances and transactions in the markets where it was introduced. Open finance initiatives and new fintech data services now extend this to broader categories such as payroll, pensions, investments, mortgages and employment data, often available in near-realtime. This higher-frequency information gives firms a clearer view of a customer’s income, obligations and goals, which in turn enables more precise and timely actions.

New legislation, including the UK’s Data (Use and Access) Act, is strengthening the foundations of this ecosystem. The Act received Royal Assent in June 2025 and is rolling out through 2025 and 2026 as different provisions take effect. These frameworks promote secure data sharing, reinforce smart data principles and require firms to use strong encryption, anonymisation and transparent consent practices so that personalisation remains ethical and compliant. Open banking itself is also improving in user experience, API reliability and adoption. What was once clunky is gradually becoming smoother and more dependable for both customers and providers.

Here are two examples of use cases we’re seeing leading firms harness:

.png)

2. Variable Recurring Payments (VRPs)

VRPs turn this intelligence into action. Beyond one‑off payments, VRPs allow customers to authorise smart, capped, and revocable payment mandates that move money when conditions are met (e.g., “sweep anything above £X to savings on payday”.) Originally developed in the UK as a part of the broader Open Banking initiative, VRP’s (or similar technologies) are being developed in the EU, Australia, Singapore, and Brazil to name a few.

Here’s what VRPs will enable in the future:

- Proactive cash‑flow management: automated bill protection, overdraft avoidance, and surplus sweeps aligned to pay cycles.

- Goal‑based automation: rules that route funds to pensions, ISAs or debt reduction based on personalised triggers.

- Cleaner consent: explicit mandate scopes make automation transparent and reversible.

3. Improving AI infrastructure

AI-driven personalisation is still early and largely experimental, but the foundations are emerging. Firms are piloting systems that combine a customer’s real-time financial data with the organisation’s rules on eligibility, risk and suitability. These systems can suggest, and eventually may take, contextual next-best actions such as warning about bills, highlighting unusual activity or adjusting savings behaviour. Actions are triggered by events such as payday or low balance, and every step is logged and explained so firms can demonstrate why it happened and whether it improved outcomes.

At the same time, Model Context Protocols (MCPs) are becoming a potential standard for allowing AI assistants to interact safely with financial tools. An assistant can request only the specific functions it is authorised to use, such as an affordability calculator, a payment initiator or an approved data source. Each request is permissioned, recorded and auditable, which helps firms meet Consumer Duty expectations on transparency and data access. Adoption is still at an early stage, but forward-leaning banks and fintechs are beginning to test MCPs in controlled environments.

Fully agentic AI is still a future goal rather than a current reality, but MCPs provide a clear pathway. As the technology matures, assistants will be able to take small and tightly controlled actions, such as adjusting savings rules or initiating VRPs, within limits set by the firm and with explicit customer consent. This opens the door to the next generation of safe and intelligent GenAI-powered financial experiences.

4. The UK Financial Conduct Authority’s (FCA) Consumer Duty

The regulatory landscape itself is also evolving, with a focus on consumer outcomes. The UK’s Consumer Duty sets a clear expectation: firms must deliver demonstrably good outcomes for customers. Complementing that is a new targeted support regime that aims to let firms provide data‑driven, context‑specific help (for example, nudges and product guidance based on identifiable factors) without crossing the full advice boundary. This opens the door for scaled personalisation that was once reserved for wealthier clients:

- Mass‑market, rules‑backed guidance that adapts to each user’s situation based on verified data and predefined rules. It brings advice-level insight to everyday customers without crossing regulatory lines.

- Clearer governance defining personalised education versus regulated advice helps firms set firm boundaries. By classifying outputs and keeping recommendations transparent, they protect both customers and themselves.

However, it also introduces risk. If consumers misinterpret these interactions as formal advice, mis-selling and remediation risk will follow. Clear communication, human intervention, and robust governance are therefore critical.

Who’s doing personalisation well right now

While many financial institutions are still talking about personalisation, a few are already delivering it - blending data, design, and contextual insight to offer experiences that genuinely understand and anticipate customer needs. 5 examples in particular stand out:

Starling Bank delivers strong personalisation by turning raw transaction data into spending insights that help customers understand their habits and anticipate upcoming bills. The bank also uses forecasts and smart nudges to guide better decisions before a customer reaches a crunch point.

BBVA applies a similar approach through its financial health diagnostic tool, which scores a customer’s overall financial wellbeing and provides personalised recommendations based on behaviours across accounts, spending and income.

Monzo demonstrates personalisation through features such as salary sorting, bill prediction and cash-flow analysis, all of which adapt to a customer’s pay cycle and spending patterns.

Cleo focuses on behaviour-driven financial coaching and uses live cash-flow data to deliver highly contextual prompts that help users stay on track.

Credit Karma has built personalised debt-reduction journeys and bill alerts that respond to changes in a customer’s financial position in near-realtime.

What comes next?

If firms can combine rich, behavioural data; AI-driven, context-aware interfaces; and robust, transparent systems - they won’t just personalise for show. They’ll build trusted relationships, improve financial outcomes, and outpace competitors who are still stuck treating personalisation as marketing lipstick.

As open finance matures, VRPs expand, and agentic AI becomes safer and more interoperable, financial services will move from reactive nudges to intelligent systems that quietly optimise on our behalf - spotting issues before we do, stitching together data from across our financial lives, and acting (with clear consent) in the background.

Ultimately, the organisations that come out on top will be those that successfully turn stressful and complex financial decision-making into calm, proactive guidance.

Tap into award-winning insights and strategies

Who better to help you research, design, and build personalised digital experiences than the five-time Consultancy of the Year? That’s right - Accenture, Capgemini, Deloitte, CapCo, and the other so-called big names lost out to “little” 11:FS because we deliver impact - that’s why our clients voted for us.

We’ve helped brands around the world launch winning digital propositions and we’re ready to help you focus your innovation efforts to become more efficient in an industry that demands it more than ever.

But that’s enough talk. Let’s get moving.